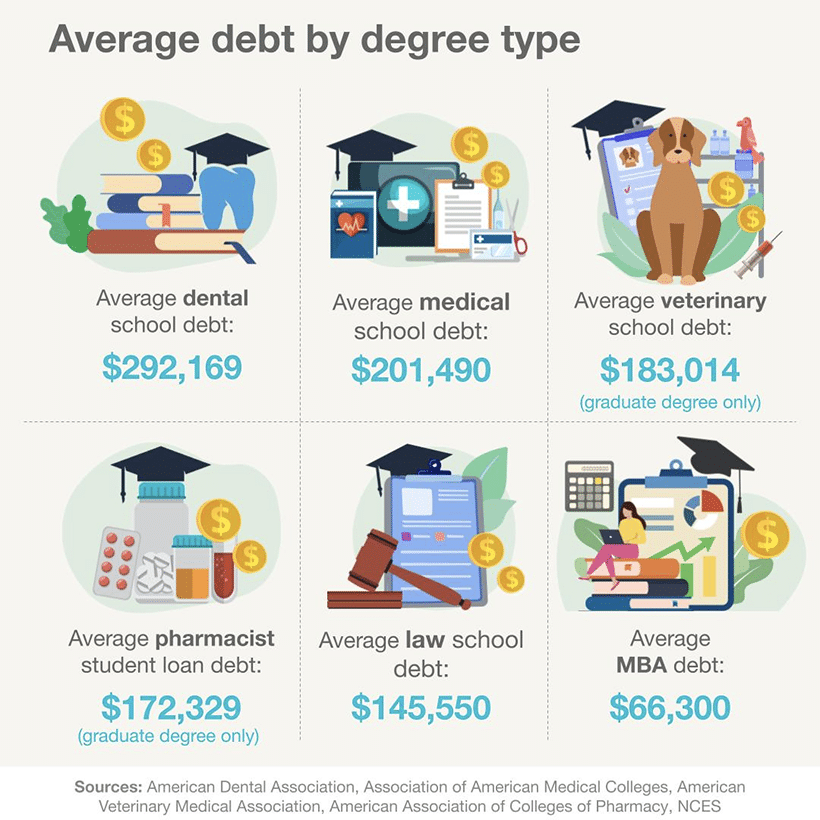

On average, student loan borrowers graduate with $29,650 in student loan debt. But college graduates with six-figure balances aren’t uncommon, especially in the medical and legal fields.

Figuring out how to pay off $100k in student loans, $200k in student loan debt, or even more can be challenging, but some repayment strategies can help you achieve your goal. While the standard repayment term for federal loans is 10 years, it takes anywhere between 13 and 20 years on average to repay $100k in student loans.

Here are some different scenarios to consider, depending on your financial situation and goals.

How common is it to have over $100k in student loans? What about $200k in student loan debt?

Currently, the average student loan balance per borrower is $29,650 — but it’s definitely a common problem to have much higher student debt in the six figures.

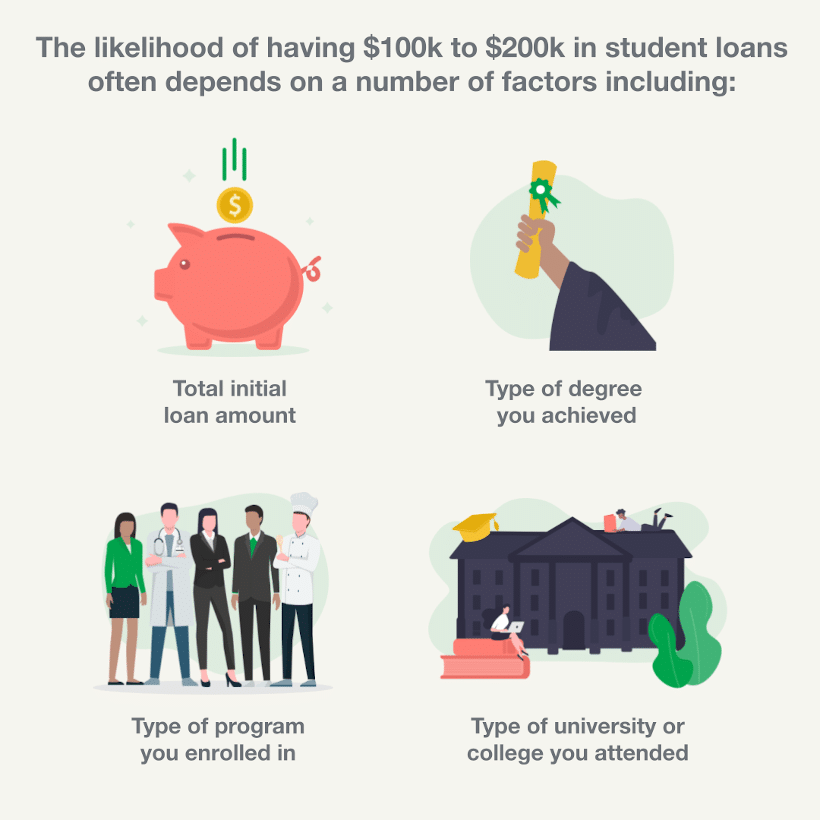

The likelihood of having $100k to $200k in student loans often depends on a number of factors including:

- How much you initially needed to take out in student loans to fund your college education (how much savings did you already have, how much federal aid did you receive, did you have financial support from family, did you get any scholarships or grants, etc.)

- The number of years you stayed enrolled in school

- The type of degrees you achieved (associate, bachelor’s, master’s, doctorate)

- The type of program you enrolled in (medical, nursing, law, business, etc.)

- The type of university or college you attended (private, public, in-state, out-of-state, etc.)

Often, those who stay in school longer to pursue advanced degrees at more expensive private universities are the people more likely to have higher student debt and be interested in how to pay off $100k in student loans or $200k student loan debt.

How long does it take to pay off $100k in student loans? How about $200k in student loan debt?

Paying off $100k in student loans or $200k in student loans depends almost entirely on two things:

- Your current student loan repayment plan

- How much extra money you have to devote to your student debt

If you have a standard 10-year repayment plan, your debt will be paid off in full in 10 years — if you don’t pay extra toward your principal or change your repayment plan.

However, there are a number of repayment options you can choose to either pay off your loans faster or lower your monthly payment.

For example, if you have federal student loans, you can opt for an income-driven repayment plan which drops your payments but extends your repayment term — causing you to take about 25 years to be debt free.

Or, if you have private student loans or a combination of both federal and private, you could always choose to refinance your student loans. Student loan refinancing allows you to customize your repayment term to be shorter, longer, or the same — while getting a lower rate to save money on interest costs.

Outside of your repayment term, another major factor is if you have extra funds to pay down your student loan balance. If you increase your monthly payments beyond what’s stated on your bill, or you use cash windfalls like tax returns and work bonuses to put toward your principal, you can pay off your loans much faster.

How does the monthly payment on $200k in student loans compare to $100k?

The total amount of your student loan payments — whether you have $100k or over $100k in student loans — will depend on your own unique loan situation. Some key factors that impact your monthly bills are:

- How many total loans and payments you have

- What your interest rate is and how much in interest you pay each month

- What the length of your repayment term is and how many months you have to pay off your debt

How to pay off $100k+ in student loans

Ready to learn how to pay off $100k in student loans or $200k student loan debt?

If you want to eliminate your debt as quickly as possible and are in a position to do so, there are a few different options to consider. Here are some of our top choices (note: this can also work if you’re trying to figure out how to pay off $200k in student loans quickly).

1. Student loan refinancing

Whether you have federal or private student loans, you may be able to refinance them with a private lender. Student loan refinancing involves replacing your current loans with one new loan.

Each lender typically has a range of interest rates you can qualify for, and if your credit and income are in great shape — or you have a creditworthy cosigner — you may be eligible for an interest rate that’s lower than what you’re currently paying.

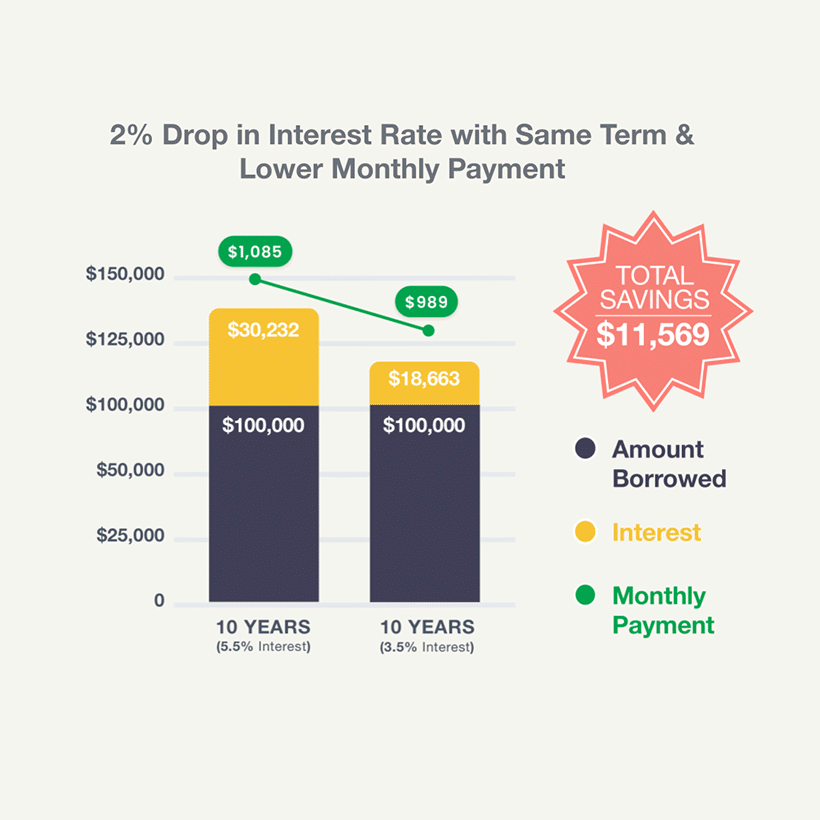

For example, let’s say you’re wondering how to pay off $100K in student debt with a 10-year repayment term and an average interest rate of 5.5%. If you qualify for a 3.5% interest rate with a private lender, refinancing would lower your monthly payment by $96, and save you a whopping $11,569 in interest.

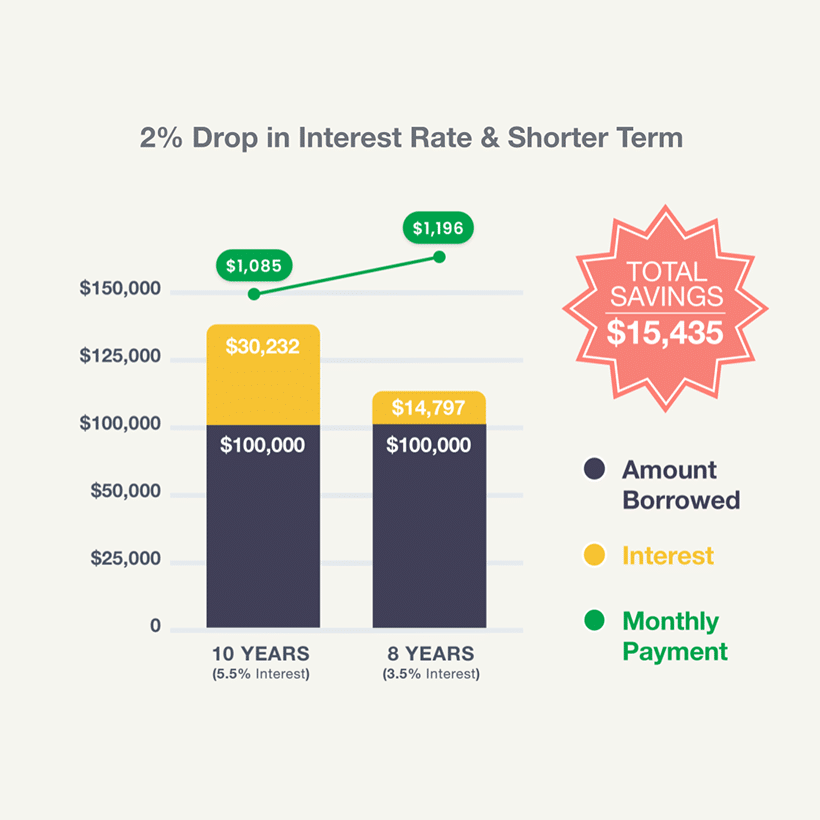

If you want to pay down your debt faster, you can also choose a shorter repayment term. For example, let’s again say you’re trying to figure out how to pay off $100k in student loans. Your repayment term is 10 years, and you have an average interest rate of 5.5% — same as the example above. In this scenario, your monthly payment would be $1,085.

If you choose an eight-year repayment term instead and qualify for a 3.5% interest rate, your monthly payment would increase only to $1,196 — but you’d save $15,435 in interest.

Note that you can also choose a longer repayment term with refinancing, which will lower your monthly payment. But doing so will also increase the amount of interest you pay over the life of the loan.

If you’re considering refinancing, be sure to compare lenders using Purefy’s rate comparison tool. With just a little information about yourself and how much you owe, you can compare multiple refinancing lenders, along with their rate offers for you, in one place.

All in all, student loan refinancing can be one of the most effective solutions for how to pay off $100k in student loans or $200k student loan debt.